- 2 Min Read / Blog / 3.2.2020

Note (January 2019): Another, newer feature that is hugely valuable in mobile banking is Face ID in financial apps.

Mobile banking has become the ubiquitous and ever-present way for consumers to interact with their banks and their investments. In fact, mobile experiences for financial institutions have become so expected that many consumers never have cause to visit their bank’s brick-and-mortar branches. Some banks, namely web-only banks like Simple and Ally, obviate the need for physical branches and ATMs altogether via mobile banking features.

Mobile experiences for financial institutions have become so expected that many customers never visit brick-and-mortar branches.

Why the paradigm shift? Like any industry, finance has recognized the user expectation for immediacy and intuitive features that are accessible wherever they need them. By recognizing user needs and addressing their mobile-first expectations, many prominent banks have successfully connected with mobile audiences and brought new utility to users on mobile. But the story doesn’t end there—banks still have massive opportunities to engage with customers on mobile and provide all-new value through native apps. Here are some of the mobile banking features that have an impact for customers.

Think beyond mobile check deposit.

With emerging technologies like Touch ID on iOS and similar fingerprint sensors for Samsung devices running Android, it’s never been easier for developers to add biometric security to their app sign-in process. Just as Apple granted developers access to the Touch ID sensor in iOS 8, Android hardware OEMs are increasingly providing ways for developers to enhance their apps’ security and bring piece of mind to privacy-conscious users.

Touch ID is only the beginning.

As Apple Watch and other wearables become more acquainted with users’ unique biometric rhythms and collect data about individual users—like the unique sound of their voice or the cadence of their heartbeat—new frameworks will doubtless be constructed to include that data in biometric authentication measures. This will provide increased security and privacy in apps across the system, but will be most relevant in banking apps that provide access to users’ most sensitive financial information.

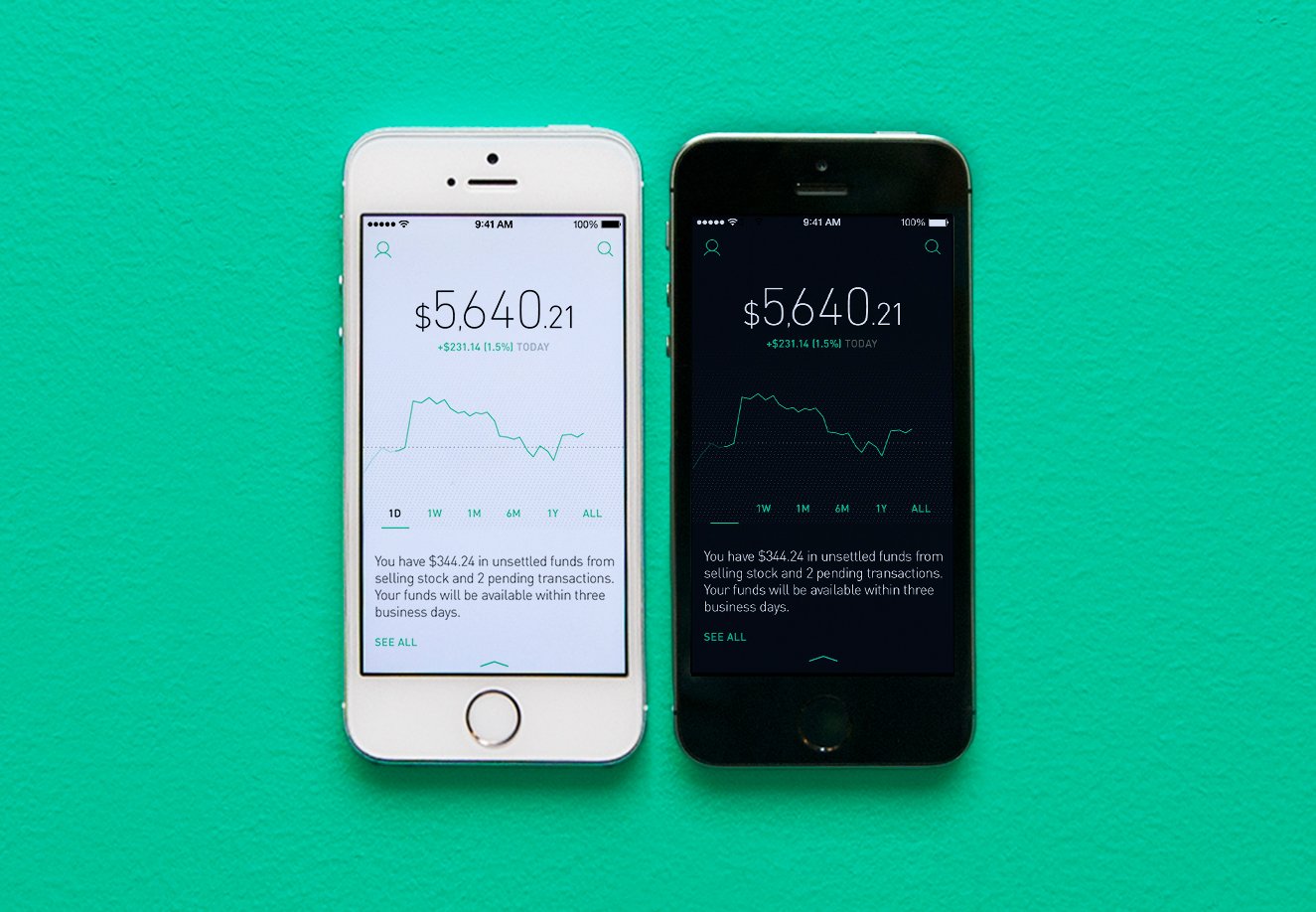

Both iOS and Android give app developers opportunities to share data with the user through venues outside of the traditional app chrome. Whether this information is conveyed through interactive notifications, widgets in the iOS Notification Center or on the Android home screen, cards within Android’s Google Now, or even through new wearable capabilities, mobile banking applications have massive opportunities to share relevant and up-to-the-minute financial information with their customers on mobile.

Users can optionally skip the lengthy sign-on process and check if they have enough in their checking account for a timely transaction.

By providing access to simple account balances in venues other than within the app, behind an authentication wall, banks can help users interact with their accounts and their money in simple and unobtrusive ways. No need for transfer capabilities or deposit functions—users can sign into their apps directly for that. Instead, these features would allow users to optionally set preferences around when and where they are presented with account balances at a glance. Some banking apps already provide this option, but third-party solutions like Level and Mint.com go further with glanceable Notification Center widgets or quick-access dashboards. As wearables and smaller connected devices become prevalent and mainstream, these features will only continue to become more relevant.

Another quick-access feature on iOS is Passbook, the virtual wallet of mobile tickets, passes, and membership cards that helps millions of people buy lattes at Starbucks or catch a movie at AMC. Mobile banking apps can provide passes for payment cards and even account balances inside of Passbook, allowing users to pay at certain retailers by scanning an on-screen barcode. Further, using Passbook as a venue for account status and balances provides further access to banking accounts right from a system-level app, and allows users to better engage with and understand their financial holdings.

Passbook isn’t just for your Starbucks card—it can also boost visibility into banking accounts on mobile.

Passbook passes are interesting because of their system-level access. Passes can be triggered by geo-fences and present themselves to users on the lock screen, allowing banks and retailers to push messaging to customers through a platform they’ve already explicitly opted into at the moment it becomes relevant. For payment cards issued by non-banks, like credit cards from retailers, the barcode capability can serve as a viable alternative to Apple Pay on iOS within Passbook.

The battle for NFC mobile payment supremacy is brewing, with entrants like Apple Pay, Google Wallet, Softcard, and Samsung LoopPay vying for control of the market. For banks, providing NFC access to payment cards and credit cards give customers another opportunity to use their cards throughout their daily routines, and even can help customers make banking decisions between different institutions based on support for a preferred platform.

For millennials and tech-savvy consumers, compatibility with a preferred mobile payments platform can determine which bank they choose or switch to.

For Apple Pay compatibility, banking institutions typically have to cooperate with Apple directly for integration to come in an upcoming release of iOS. For Android-based mobile payment platforms, most payment cards will work out of the box, regardless of the issuing bank or creditor. Whether payments are processed via NFC contactless payment terminals, or via QR code scanning like CurrentC, banks can help consumers leverage their smartphones in new and useful ways no matter where they like to shop.

Users expect digital experiences to have parity with real-world institutions, and increasingly demand mobile experiences have feature parity with companies’ web counterparts. If users can open and close accounts in person, make adjustments to their balances over the phone, or tweak their email notification preferences in the web interface, they expect all these features to be equally possible through a mobile app.

Users expect real-world and web-based features to be possible through a mobile app.

Just as maintaining feature parity between desktop and mobile versions of a web application is important, understanding users’ demands for feature parity between the branch, web, and native apps is critical to a successful financial app on mobile. Users become understandably frustrated when common tasks are hidden or disabled based on their device form factor, and will only continue to expect new capabilities as mobile devices become more prevalent and powerful. Building mobile experiences that account for user behaviors and expectations—and providing adequate support for users directly in the app—is crucial for success on mobile.